The last 13 years have brought about land-slide changes for the commercial aviation industry and especially airlines in particular. Ever since deregulation the biggest problems facing the industry have been over capacity and irrationality.

Over capacity was inevitable in many respects, however there are two types of over capacity. The first type of over capacity is structural over capacity. Structural over capacity is that which is generated as a result of carriers’ networks (in relation to too many carriers) and technological limitations. Technological limitations persisted for a long time as aircraft for long range and ultra-long range flights were limited to 747s for many years. Which in many cases were too large to efficiently serve those markets.

Technological over capacity has been greatly abated today with smaller long range aircraft such as the 767, A330 and 777. That leaves us with network generated over capacity to contend with. For airlines to generate strong performance and support large international flights, they must be able to aggregate traffic. For example, Evansville, Indiana (EVV) for instance does not have anywhere near the market size to support a nonstop to London (LHR) flight. The annual demand for seats between EVV and LHR might be 50 passengers a year. This couldn’t support a single flight a year, let alone daily service. So airlines take traffic from all over the country or the world and funnel them through a few large airports so that they can fill the daily or in some cases several times a day LHR flight(s). The more carriers that exist, the more hubs exist, and the more non-stop operations there are. However, this leads to over capacity.

As airlines began to grow after deregulation, it became necessary to have hubs in multiple geographic areas. This would allow for more opportunities to aggregate traffic, as well as to build elite customer bases. In 2000 the following airports had hub status, ATL, BNA, CVG, CHI, CLE, CLT, EWR, DFW, DTW, MEM, MIA, MSP, PHX, RDU, STL, SLC, SFO. Add those to other large markets like NYC, SEA, LAX, etc. that also had many nonstop flights. Many of these markets could not support that many nonstop flights on their own.

In the last 7 years or so there have been several rounds of large mergers in the industry. US Airways and America West merged, then Northwest and Delta, to be followed by United and Continental. This has allowed carriers to reduce flights to better match supply with demand. This allows for significantly less spoilage to occur in the marketplace. The higher load factors give carriers more revenue, while reducing the costs of operation leading to higher margins.

Capacity rationalization has had a predictable result. Airlines have refocused on their most viable hubs. This has resulted in the loss of a lot of direct service out of former hubs. STL, RDU, CVG and MEM have been pared down to mainly hub-to-hub service, or what we call flow-hubs. In many cases there hasn’t been a significant drop off in traffic, as capacity still remains within the networks for passengers to get to where they need to go via single connect. These markets are still very important to airlines as there are significant elite customer bases in those airports, and therefore significant high-yielding business traffic. This explains why there has been relatively limited encroachment of competition in these markets.

Let’s take a look at two different examples, Cincinnati (CVG) and Memphis (MEM). Both airports served as major hubs for their respective carriers before their merger, CVG for Delta and MEM for Northwest.

CVG was Delta’s foray into the Midwest, and their only Midwestern hub. Because Delta was very Atlanta-centric, they needed a point in their network to funnel traffic from the northern parts of the country. In many cases a connection in ATL did not make geographical or routing sense for passengers. So they could accommodate them through CVG. CVG, however is the exception rather than the rule. Firstly it is well within the catchment area (area where local origination and destination traffic can be gathered) of several other airports, and secondly Delta used it a largely a hub for Comair (a regional partner). Regional jets have significantly higher unit-operating costs, so an unbalanced hub (between regional and main-line service) is at high risk to spikes in fuel prices.

The following data is from the BTS and is comprised of all airlines operating flights at the respective airports.

Courtesy of the BTS.

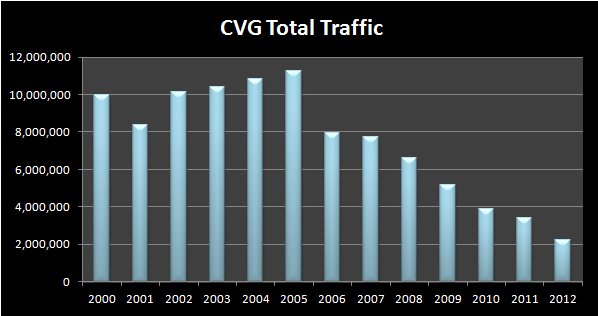

This chart that shows CVG’s total traffic paints an interesting picture. Data for 2012 is not complete. CVG peaked in 2005 right around 12mln passenger enplanements. Then the hub was scaled back well before the merger, due to low load factors as well as the high concentration of regional jet operated flights and its proximity to other major airports contributed to its demise. Most notably, Detroit (DTW) and Chicago O’hare (ORD) had significantly more direct service within the catchment area than CVG.

Courtesy of the BTS

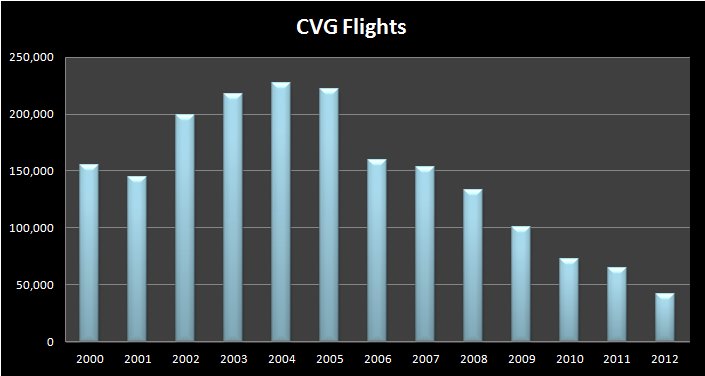

Again, the number of flights operated repeats the same story as before.

Courtesy of the BTS

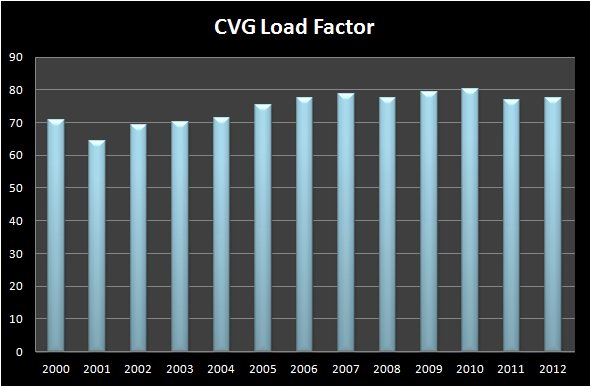

Load factor which is a the percentage of seats filled on an aircraft is measured at the unit level, Revenue Passenger Miles (RPM)/Available Seat Miles (ASM). What it shows is a seemingly slight up-tick in load factor since the hub was scaled back starting in 2005. Where CVG also benefits from is the fact that more of the flights are being operated on mainline equipment or larger 76-seat regional aircraft which have substantially lower unit costs than the 44 and 50 seat regional jets that Comair operated out of CVG.

Given the size of the CVG metro area (around 2mln) the data indicates that there is some potential for traffic aggregation (around 2mln assuming 1 flight per person per year). Although it is now where near where it was in 2005 where that same factor would be multiplied by 5 for ~10mln connecting passengers. CVG was simply massively over served due to the structural requirements of Delta’s pre-merger network, and a lack of rationality on the part of their Revenue Management and Network Planning departments.

Memphis (MEM) had some similarities for Northwest. Northwest, unlike Delta had a very northern and Midwest/heartland centric network. While Delta had a stronghold in the southeast, Northwest before its merger with Republic had no such stronghold. Through Republic they gained Memphis. Memphis served to aggregate southeastern traffic and feed Minneapolis and Detroit with a secondary emphasis on nonstops out of Memphis. Memphis’ capacity was more rational that the capacity that Delta threw into CVG, due in part to the diligence of Northwest Revenue Management and Network Planning departments (which were the envy of the industry at the time), but also due in part to its proximity to ATL, a megahub.

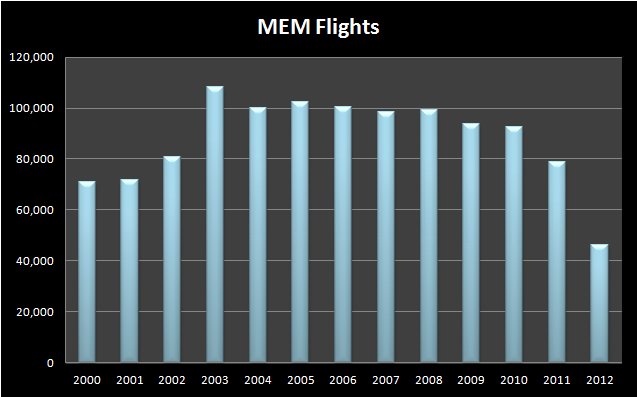

Courtesy of BTS data for 2012 is incomplete

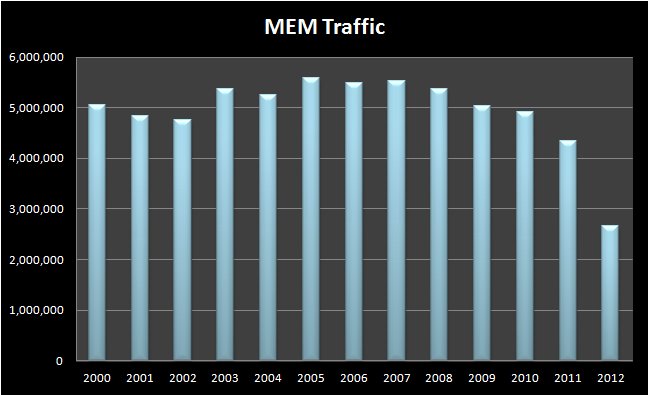

MEM peaked at about half the size of CVG, however, even after capacity rationalization has suffered nowhere near the traffic loss that CVG did. As of July 2010 the Memphis metro area had a population of about 1.3mln, compared with Cincinnati at around 2.1mln. Part of the reason MEM has retained such high passenger traffic, despite having a significantly smaller metro-area population is that there aren’t as many other major metro airports within its catchment or drive-divert area.

Courtesy of BTS 2012 data is incomplete

Flights operated reaffirms the story that traffic is telling us. MEM has seen significant cuts to weekend flights, while maintaining weekday flights, which indicates strong business traffic demand.

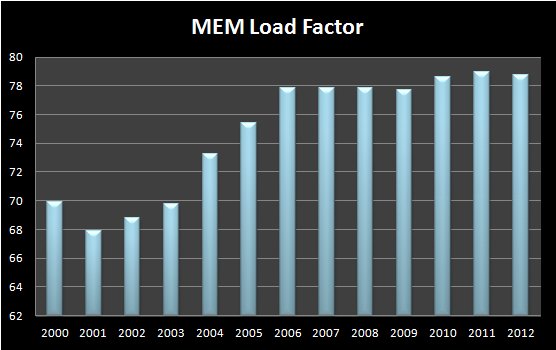

Courtesy of BTS

MEM has seen significant improvement in load factors over the years. Capacity reductions have helped to push the airport load factors to near 80%. MEM capacity rationalization in terms of load factor, flights and traffic has been much smoother than CVG has been. MEM load factors indicate an emphasis on capacity rationalization starting back in 2002. This is the result of more rational actions taken by the market-leading carrier than was the case in CVG, as well as steadier demand.

In any case if you take a trip through either airport on a weekend, it will seem like a ghost town. With only the airline signage to remind you that they were once flagship hubs in both of their respective pre-merger networks. A similar scenario has unfolded at STL, RDU and BNA as well. CVG and MEM also serve as indicators as to what will likely happen in the US Airways and American Airlines merger. US’s hubs in Charlotte (CLT) and Phoenix (PHX) will likely be scaled back significantly. PHX serves as US’s west coast hub, but in the greater context of the merged network will be nowhere near as significant as LAX. Plus PHX has a much lower fare environment due to the significant presence of Southwest there. CLT, likewise is sandwiched between CHI and MIA and will likely be reduced to a flow-hub (like CVG or MEM). While this means less nonstops for passengers originated or terminating in those markets, they will be able to get anywhere with a single or double connect. What it does mean is a more stable and rational market environment for all carriers involved.